In the past, banks built themselves from the inside out—and for decades, it worked. Products were developed around a sturdy core banking system and rigid business process to ensure security and trust, distributed through branch networks, and only

then wrapped in a customer experience and brand veneer. But those days are over because customers and the market demand the opposite. Today’s Fintech upstarts and digital-first neobanks have flipped the model on its head, designing their institutions from

the outside in. To stay competitive in the digital age, traditional banks will have to consider the unthinkable: turning their entire business architecture upside down.

In the pre-digital era, banking products were largely undifferentiated commodities. Most institutions offered the same accounts, loans and transactions, competing mainly on interest rates and fees. Banks were built from the core outward—strengthening balance

sheets, managing risk and scaling distribution—while customer experience was often an afterthought, since alternatives were limited.

High barriers to entry reinforced this model. Building a bank required heavy investment in branches, licenses, compliance, staff and years of preparation, which kept competition slow and scarce.

The digital era has dismantled those barriers. Fintechs can launch in months using third-party tech stacks, APIs and cloud platforms instead of decades of infrastructure. Even individuals can issue tokens or digital assets in minutes. The only real requirement

now is delivering clear value to a customer segment.

This digital shift has intensified competition. Customers can switch providers with a few taps, and they expect seamless experiences, emotional connection and alignment with their values. Competing on process and price alone is no longer enough. Traditional

banks cannot afford to remain massive turtles trying unsuccessfully to get up from their backs onto their feet in the digital world.

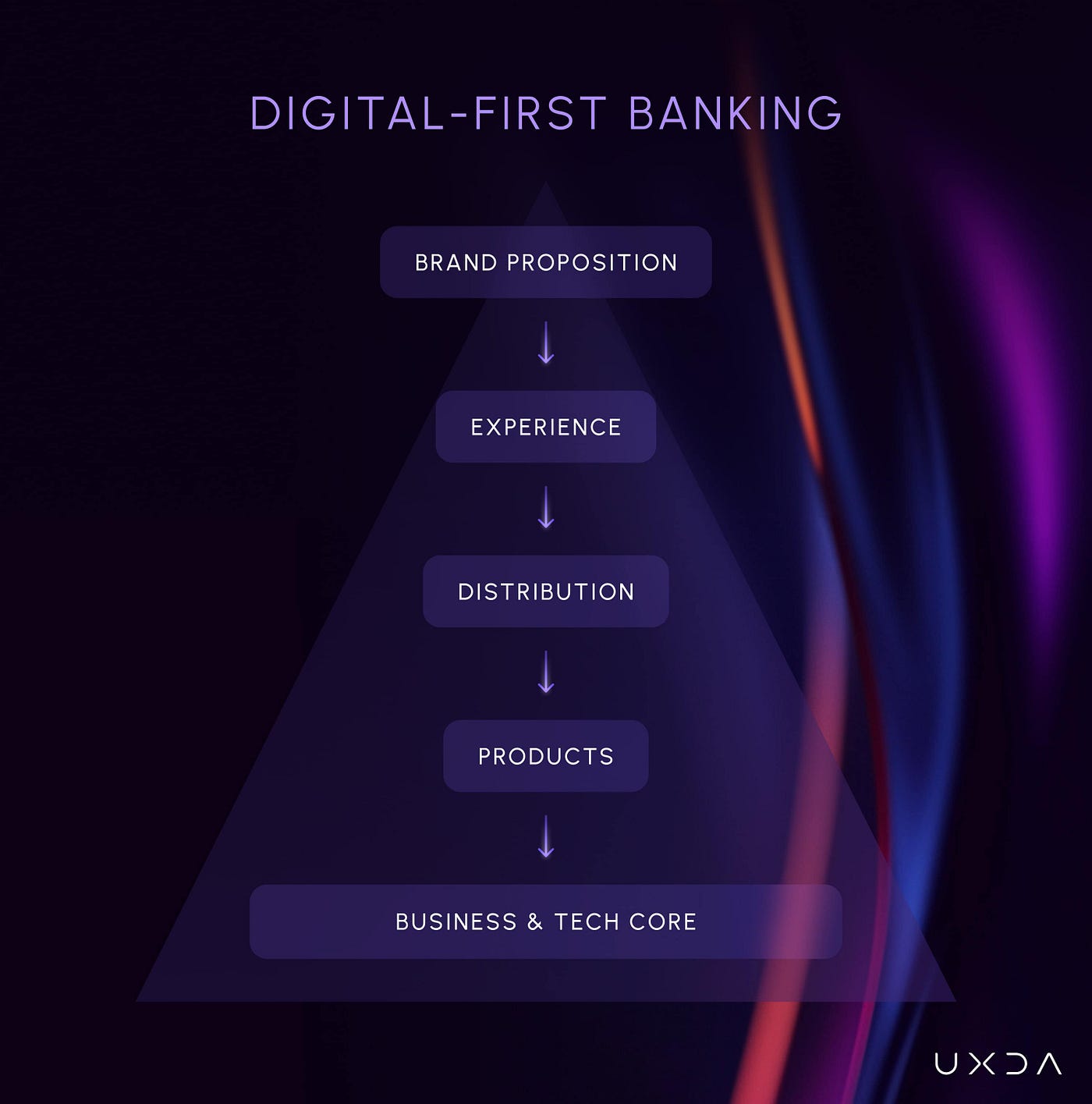

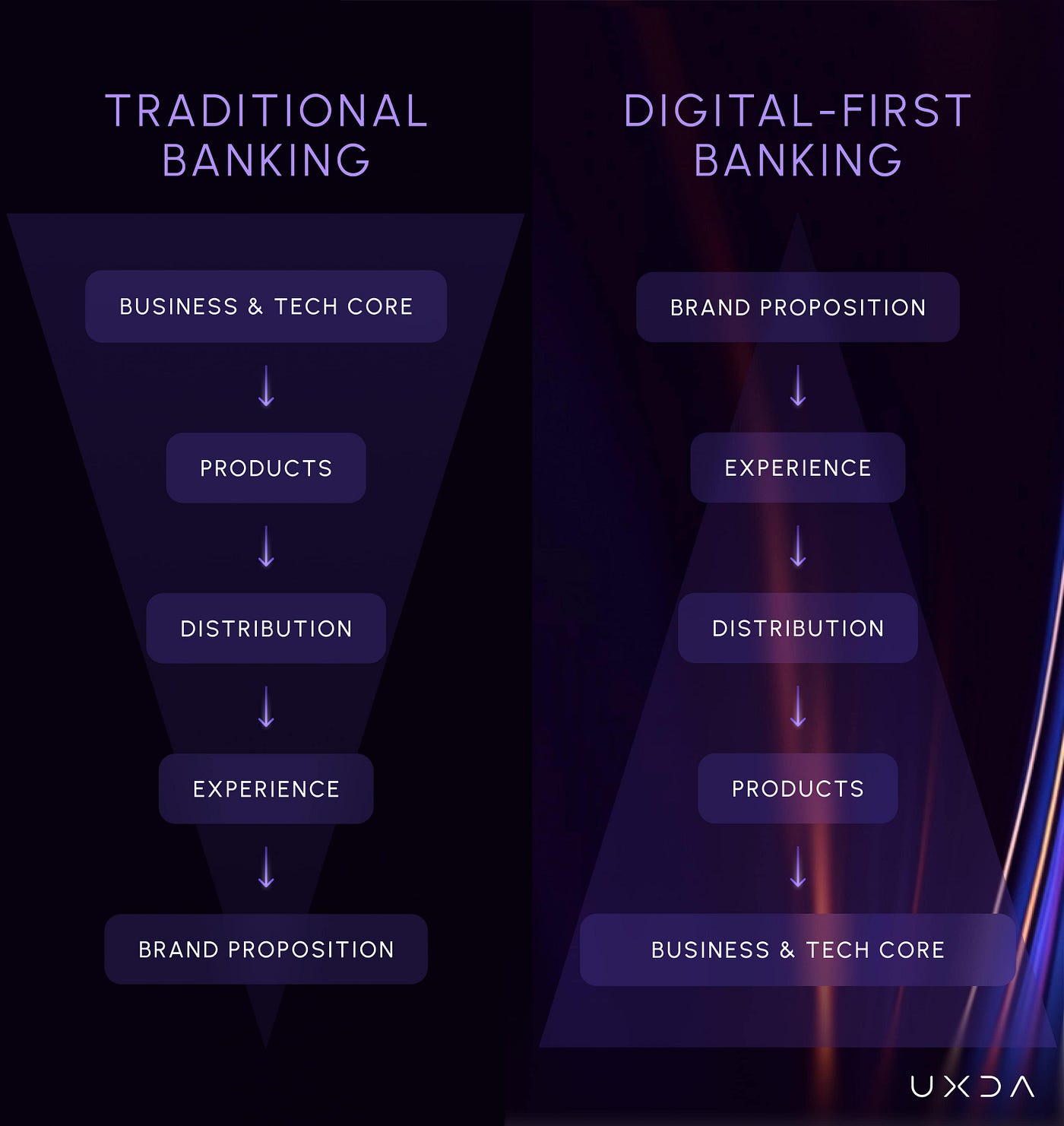

Traditional banks still operate inside out—starting with internal systems and processes, then building products, distribution, experience and, finally, brand differentiators. Fintechs and neobanks invert this logic. They begin with brand purpose and customer

promise, design engaging experiences, choose distribution that meets customers where they are and then build products and core technology to support that ecosystem.

What differentiates challengers is not a new app or feature, but a radical inversion of business logic. To stay relevant alongside tech giants and digital-first competitors, banks must shift from compliance-first to purpose-led, from process-driven to genuinely

customer-centered. That requires rethinking legacy systems, governance and culture—placing customer experience at the core of strategy, not at the periphery.

Traditional Banking Architecture: The Inside-Out Model

Traditional banks are built from the inside out — structured around internal systems, product silos, and compliance-first processes. Each layer (Core → Products → Distribution → Experience → Brand) extends outward from operations, projecting

the bank’s internal logic onto the customer.

This architecture prioritizes control, stability, and risk mitigation. It ensures reliability but slows innovation, creating silos and checklists that suppress agility. Front-line employees follow scripts, and “innovation” happens in isolated

labs, not across the organization.

In this model, customer experience is secondary. Products and processes come first, and customers are expected to adapt to them — leading to lengthy forms, fragmented services, and friction from compliance-heavy flows. The result is consistent

reliability but inconsistent experience.

The logic follows a clear pattern:

- Core dictates offerings: Legacy cores limit flexibility, forcing one-size-fits-all products.

- Product-centric structure: Success is measured by internal P&L, not unmet customer needs.

- Distribution before experience: Channels mirror internal processes rather than customer journeys.

- Experience as an afterthought: UX is layered on top of rigid systems instead of designed around people.

- Brand as veneer: Marketing promises “customer-first” while digital touchpoints reveal outdated systems.

This model made sense in the pre-digital era of limited alternatives and physical branches. But in today’s digital economy, where customers expect seamless, personalized experiences, the inside-out approach exposes its limits — showing why

banks must now rebuild from the outside in.

Next-Generation Digital Banking Architecture: The Outside-In, Purpose-Led Model

Fintechs and digital-first banks flipped the traditional model by building from the outside in — starting with purpose and customer promise, then shaping experience, distribution, products, and finally the core. Their logic: understand

what customers value, deliver it beautifully, and build systems to support that.

Their culture is customer-led and innovation-driven. Teams from tech and e-commerce backgrounds work in flat, agile structures guided by purpose, not process. Success is measured by NPS, engagement, and loyalty — not just profits. Risk is

managed dynamically through tech and experimentation, enabling safe innovation.

- Purpose & Brand Drive Strategy

Fintechs begin with a mission — e.g., “make banking fair” or “help people save confidently.” The brand defines every decision, ensuring actions align with customer purpose rather than internal process. - Experience First

User experience is the product. Every interaction — from onboarding to support — reflects the brand’s values and emotional tone. Compliance and security are seamlessly embedded, not imposed. The goal: frictionless, human, and emotionally resonant journeys. - Customer-Led Distribution

Channels are built around customer habits, not institutional needs. Digital by default, neobanks ensure seamless omnichannel access across app, web, or partner ecosystems (e.g., Banking-as-a-Service). - Agile, Needs-Based Product Development

Products evolve from customer insights, built and tested rapidly by interdisciplinary teams. Feedback loops and data analytics fuel continuous improvement. Compliance is integrated early, making innovation both fast and safe. - Flexible, Modern Core Technology

Cloud-based, API-first architectures replace rigid legacy systems. Modular, real-time, and scalable cores support personalized, instant, and connected experiences — enabling partnerships and rapid feature releases.

In essence, the outside-in model redefines banking around people, not processes — proving that purpose-led design and profitability can coexist when experience becomes the true core of the business.

Implications on Strategy

Strategy formation diverges with architecture. Inside-out banks plan from capabilities outward, tweaking for customers only when pressured. Outside-in banks start with customer goals and purpose, then align capabilities to deliver distinctive

value.

For incumbents, adopting outside-in means redefining success beyond financials to include customer metrics and being willing to disrupt existing products. A practical path to this shift follows later.

1. Traditional Bank Strategy: Product and Efficiency Focus

Planning extends what exists: grow volumes, cut costs, meet regulations. Strategy anchors to assets and favors product, pricing, and distribution plays. Roadmaps are multi-year and waterfall, with low risk appetite that protects the status

quo. Customer experience is cited in vision decks but rarely drives decisions, so “customer-centric” plans often become familiar product pushes and generic experiences tied to internal metrics.

2. Digital Bank Strategy: Customer and Differentiation Focus

Strategy begins with market insight and target segments: identify needs, solve pain points, and differentiate through experience. Growth follows from delivering unique value. Plans are iterative and flexible, updated as data and feedback

emerge, enabled by agile teams and modular tech. The aim is outside-in value creation — serving a niche or broad need better than anyone else through superior experience and technology.

3. Competitive and Market Approach

Incumbents view competition as share defense against other banks and fintech, leaning on regulation, acquisitions, or pricing power — often missing comparisons customers make to top tech experiences. Digital players benchmark against the

best experiences in any industry and use ecosystem partnerships and embedded finance to outpace expectations, not just rivals.

4. Metrics and KPIs

Inside-out institutions prioritize product sales, volumes, branch performance, and compliance; customer measures appear but rarely rule. Digital-first banks elevate NPS, churn, daily active use, and lifetime value alongside financials, aligning

incentives to relationship depth and engagement rather than short-term product sales.

Implications on Product Development and Innovation

Architecture shapes how banks build. Inside-out institutions behave like heavy ships — safe but slow — while outside-in challengers move like a fleet of speedboats. Many incumbents adopt “agile” labels, yet dependence on yearly core releases

and committee approvals throttles velocity. Real agility requires architectural inversion and empowered teams.

1. Traditional Banks: Waterfall Development and Siloed Innovation

Legacy banks still run long, waterfall cycles with fragmented handoffs and compliance gates, so products launch late and already lag user needs. Stability trumps iteration; UX work crawls through sign-offs; labs sit at the edge, producing

prototypes that struggle to integrate with the core. Governance layers dilute bold ideas, yielding apps that digitize paper processes instead of redesigning them. With rigid cores, three-quarters of banks say they can’t improve UX quickly, and transformation

arrives as one-off projects that lose momentum.

2. Digital Banks: Agile Development and Continuous Innovation

Outside-in players treat development as perpetual. Cross-functional squads ship frequently, watch feedback in real time, and refine continuously. They prioritize features that solve customer problems — like instant card controls — over internally

convenient upgrades. “Test and learn” rollouts de-risk change, while high deployment frequency turns releases into steady improvement. When new enablers appear — such as open banking — they integrate fast because it’s useful to customers.

3. Governance and Product Risk

Incumbents gate compliance at the end; digital banks design with it from the start. Embedding risk and compliance into product squads enables “compliance by design,” producing flows — like streamlined KYC — that are both safe and smooth.

This integration reduces friction and speeds approval, something legacy structures struggle to match.

4. Time to Market and Adaptability

Slow cycles cause incumbents to miss windows and defend sunk costs. Digital banks move first, measure, and pivot or retire features quickly. That adaptability, powered by outside-in priorities and modern stacks, turns innovation into a daily

habit rather than a periodic program.

Implications on Technology and Infrastructure

Technology defines the speed and shape of change. Inside-out banks carry aging cores, fragmented data, and rigid stacks that make adaptation slow and costly. Outside-in players build on flexible, modern platforms, iterating fast, integrating

easily, and scaling efficiently — turning IT from a cost center into a growth engine. Without core modernization or smart layering, digital transformation stalls; many failures trace to sleek front ends still tethered to legacy cores that can’t support real-time,

personalized, omnichannel services. Hence the “heart transplant” imperative: daunting, but necessary to flip the model.

1. Traditional Banks: Legacy Core and Integration Complexities

Most incumbents run monolithic cores built for robustness and batch processing, not agility. Even small changes ripple across a maze of add-on systems, creating data silos and limiting real-time views. Development slows under interdependencies

and scheduled downtimes — unacceptable in a 24/7 world. Scalability demands expensive hardware, pushing run costs up. The majority of IT spend goes to maintenance, starving innovation and time-to-market. Heavy reliance on a few core vendors restricts differentiation,

while kludgy middleware is often required to connect with modern services.

2. Digital Banks: Modern, Modular Tech Stack

Digital-first banks start cloud-native and API-first, using microservices that deploy independently for speed and resilience. Continuous, no-downtime updates support perpetual improvement. Configurable cores accelerate product launches; open

APIs extend reach through partners and embedded finance. The result is elastic scale, rapid integration of new capabilities, and a platform posture that compounds value.

3. Security and Compliance Infrastructure

Both must be airtight, but approaches differ. Inside-out banks lean on heavy, manual processes that slow change. Outside-in players build “compliance by design,” automating controls from code scan to infrastructure, and offering user-level

security controls that boost trust without adding friction. Cloud security features, when properly managed, deliver strong protection while preserving agility.

4. Technical Debt vs. Technical Advantage

Incumbents carry layers of point solutions bolted onto legacy cores, consuming budgets just to keep lights on. Challengers concentrate spend on new value, not upkeep. Some incumbents pursue modern cores or parallel digital stacks to phase

out the old, but until architecture truly shifts, cost structures remain high and margins squeezed. Modular tech lets challengers adopt new protocols and AI quickly; incumbents often follow late due to integration drag and cultural caution. In short, architecture

determines pace: tech debt locks you into yesterday; modular platforms let you ship tomorrow.

Implications on Customer Relationships and Engagement

Customer relationships diverge sharply by architecture. Inside-out banks bolt engagement onto legacy stacks; it feels add-on and fragmented. Outside-in banks make engagement the product itself — daily, helpful micro-interactions that build

affinity. Think formal handshake versus continuous digital conversation.

1. Traditional Banks: Transactional and Intermittent Relationships

Engagement is episodic and process-led: customers show up to complete tasks, then disappear. Reliability builds basic trust, but friction, rigid policies, and limited personalization keep the relationship utilitarian. Many stay from inertia,

not love, as clunky journeys and bureaucratic touchpoints dampen loyalty.

2. Digital Banks: Engaged and Holistic Relationships

Engagement is continuous and contextual: real-time alerts, intuitive tools, plain-language support, and proactive tips make the bank a daily partner. Personalization at scale turns data into timely help, strengthening emotional connection

and advocacy.

3. Trust and Transparency

Incumbents lean on longevity and security yet often feel misaligned with customer interests. Digital players earn trust through clear pricing, in-app controls, instant visibility, and swift resolution — embedding safety without burden.

4. Community and Feedback

Outside-in banks co-create with users via forums, betas, and in-app feedback, keeping the roadmap aligned with needs. Legacy banks tend to decide in boardrooms, so changes feel distant and delayed.

5. Loyalty and Retention

Experience is the new loyalty program. Consistently convenient, helpful journeys drive consolidation, referrals, and lifetime value; friction drives churn. As customers increasingly judge banks by their digital touchpoints, retention hinges

on adopting the outside-in model.

The Transformation Challenge: Inverting the Model from Inside-Out to Outside-In

Shifting from a traditional architecture to a digital, outside-in model is like turning a supertanker into a speed boat on the go. It demands reworking operating model, culture, and systems — not just new tech or a refreshed app.

Many costly “digital transformations” underdelivered because culture, legacy integration, or execution gaps were ignored. Success comes from a holistic, multi-year approach that treats transformation as ongoing, often augmented by external

partners and new talent.

A common tactic is a “two-speed” path: keep the core running while a faster digital engine explores new ways of working. Done well, it catalyzes change; done poorly, it becomes an isolated island. Ultimately, banks must shift from operational

efficiency to design-led empathy and experimentation. Culture determines whether technology moves the needle.

- Cultural and Organizational Inertia: Habits, incentives, and hierarchy anchor the old way of working. Innovation may have been discouraged, making teams wary of risk. Change requires top-down

vision, new talent, and retraining, plus cross-functional teams that seed new norms. Resistance is real — silo leaders defend turf, middle managers fear loss of status, and control functions worry about speed. Culture must shift alongside tech, or new tools

will be absorbed by old mindsets. - Legacy Core Systems and Tech Debt: Modernizing legacy cores is heart surgery. Options include full replacement, progressive modularization around the core, or building a parallel digital stack

and migrating over time. None are easy or cheap, but delaying raises costs and constrains agility. Embracing cloud, APIs, and microservices decouples customer innovation from core transactions and enables near real-time, scalable services. - Siloed Product and Business Structures: Product and channel silos must give way to structures organized around segments or end-to-end journeys. This reorg reshapes governance, budgets, and roles,

exposing overlaps and forcing consolidation. Decision-making should center on the whole customer journey, not individual products, with genuinely empowered cross-functional teams to avoid new bottlenecks. - From Compliance-Only to Balanced Purpose and Compliance: Risk and compliance move from late-stage gatekeepers to partners embedded from day one. “Compliance by design” means co-creating safe,

usable solutions within sprints, shifting the dynamic from saying no to enabling responsible yes. - Short-Term vs. Long-Term Focus: Transformation is a multi-year investment that can dampen near-term results, tempting half-measures. The greater risk is inaction as digital players raise the

bar. Leaders must take calculated risks now to secure future viability. - Employee Skills and Change Management: Banks need more product, data, and UX capability — and fewer manual, process-only roles. Reskilling, smart hiring, and careful integration of digital talent

are essential. Clear vision, visible quick wins, and co-creation with employees build momentum and reduce fear. - External Constraints: Regulation and operational stability can’t pause for change. Major shifts require parallel runs, strong controls, and close regulator engagement. Incumbents must modernize

while staying fully compliant — open-heart surgery at marathon pace.

Conclusion

Banking is at a turning point: the inside-out model that once ensured stability now constrains growth and erodes trust. The legacy sequence (Core → Products → Distribution → Experience → Brand) versus the outside-in approach (Brand → Experience

→ Distribution → Products → Core) signals a different philosophy of what a bank is and whom it serves.

Traditional banks excelled at process and compliance, but often sacrificed flexibility and satisfaction. Digital-first players show that a purpose-led, customer-centered model is a competitive advantage, delivering higher loyalty and faster

innovation.

For incumbents, the mandate is to reimagine every layer:

- Core to Brand: let promise and purpose drive technology and processes, not the reverse.

- Products to Experiences: organize around journeys and outcomes, not silos.

- Channels to Customers: treat digital as the primary branch and be wherever customers are.

- Compliance to Purpose: embed compliance in design so safety and innovation reinforce each other.

This shift spans strategy, product, technology, and culture — replacing long, inward roadmaps with agile cycles guided by real customer insight. Customers are choosing providers that offer ease, transparency, and values alignment.

Incumbents still hold powerful strengths — scale, trust, regulatory expertise, and capital — but must fuse them with startup-level agility and customer focus. The opportunity is larger than competitiveness: an outside-in model realigns banking

with its purpose — helping people and businesses thrive.

Where development was slow and inward, an outside-in approach makes it agile and experimental, cutting time-to-market and meeting actual needs. The choice is urgent but hopeful: those who act will set the new standard — resilient, human,

and future-ready.