“Bottomed out but not rebounding” is the simplest way to describe the global agri-foodtech investment landscape in 2025, according to the latest report by AgFunder.

The eagerly-waited “barometer” of investor confidence was released last week at the World Agri-Tech Innovation Summit in San Francisco and while it reveals largely flat levels of investment ($16.2bn as compared with $16.7bn the previous year), new trends and behaviours are emerging.

Bio-based and farm management leading the “upstream” pack

The Agfunder analysis distinguished between “upstream” deals and technologies (pre-farm gate) and “downstream” (such as e-grocery and retail).

In the upstream category, companies developing solutions in bioenergy and biomaterials proved most attractive to investors globally, followed by agbiotech and farm management, sensing and “internet of things.” It will be interesting to see how this changes next year with the current geopolitical instability impacting fuel and fertiliser prices.

The UK – holding the line….. just!

In 2025, UK companies raised a collective $685M across 111 deals, representing a modest increase on the previous year. The UK is now sitting 5th in the global ranking, just below the Netherlands, with China and India taking 3rd and 2nd places respectively. Top spot, unsurprisingly, goes to the US which, despite leading the pack, is still down 8%.

The Netherlands reported a massive 44% increase in investment, taking it to 4th place and ahead of the UK by a nose.

There is a health warning to the data for the UK, however, that it most likely doesn’t include the recent hot-of-the-press news about the massive raises by Tropic Biosciences of $105M and Resurrect Bio which secured $8.1M in its recent Series A round. Impressive performance indeed which is likely to make the 2026 data look healthier. A salutary reminder that, as in the case of the Netherlands, one major deal can significantly influence the rankings.

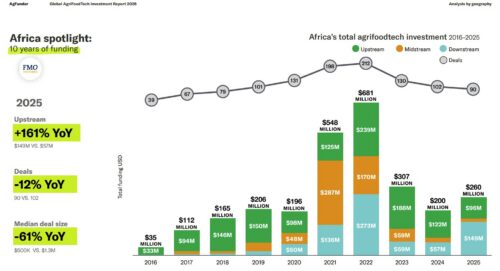

The Rise of Africa, Debt Financing and New Entrants

Despite the global appetite being cautious and focussing on clear paths to revenue and real unit economics, the entrepreneur’s optimism is still palpable with new companies continuing to emerge. For the first time since records began, the proportion of investment into “first-time funded” companies has increased – to 46% of the total global investment (an increase of around 6% on the past two, stagnant, years).

Also on the up is investment into African companies, with an increase of 30% to $260M across 90 deals. The biggest categories are Agmarket places and fintech, as well as home cooking.

Debt financing is also on the up compared with previous years, with around 18% of total investment coming from debt. This is more than double the proportion since records began, posing some interesting questions about the role of banks and providers of debt finance in leveraging different behaviours and incentives.

Future opportunities for the UK?

It’s hard to compete with the scale of India and China and the depth of capital in the US. Innovations targeted at mass markets are going to be hard to secure compared with those emerging from these behemoths. Specialised, high value innovation such as agbiotech harnessing genetic and molecular based solutions, as well as robotics and automation remain among the UK’s USPs.